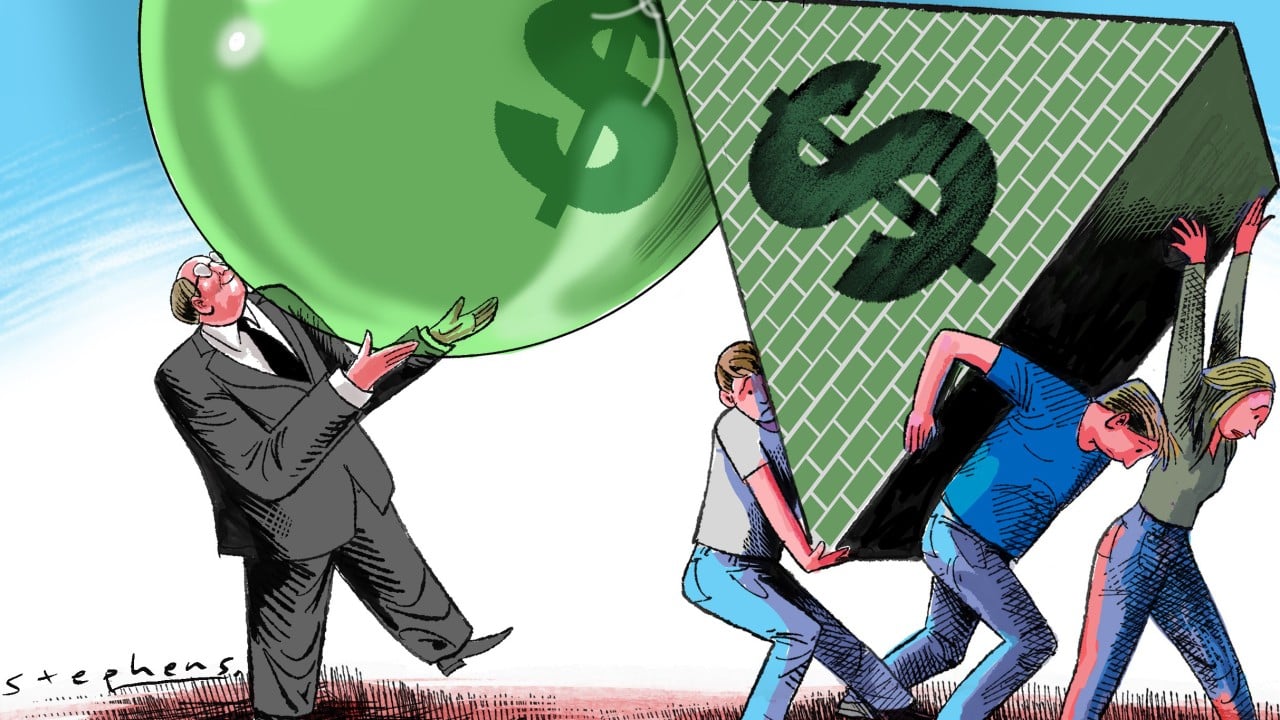

A healthy economy requires productive investment to thrive, yet modern finance is addicted to inflating asset bubbles and constructing debt pyramids. This reliance on cheap credit and soaring valuations creates a mirage of prosperity while starving the real economy of capital. When paper wealth outpaces actual industrial and technological output, a crash becomes inevitable. To fix this, policy must pivot away from subsidizing speculation and toward rewarding genuine, tangible productivity.

The Mechanized Engine of Phantom Wealth

For decades, central banks and financial institutions have operated under a flawed assumption. They acted as if pumping liquidity into capital markets would automatically trickle down into factory floors, research labs, and worker paychecks. It did not. Instead, that liquidity pooled at the top, inflating the value of existing assets like real estate, equities, and complex financial instruments.

We are witnessing a structural decoupling. Real economic growth relies on a simple formula. You combine labor, raw materials, and capital to create a product or service that possesses more value than its component parts. This is wealth creation. What we have right now is wealth extraction.

Consider how corporate behavior shifted. In a previous era, a company that generated substantial profits poured that cash back into research and development, built new facilities, or hired more specialized workers. Today, a massive share of corporate cash flows is diverted toward share buybacks. By purchasing their own stock, companies artificially reduce the supply of outstanding shares, driving up the price per share.

Executive compensation is heavily tied to stock performance. This setup creates an immediate incentive to prioritize short-term market optics over long-term industrial viability. The money disappears into the financial ether, leaving the company less resilient to future shocks.

The Anatomy of the Debt Pyramid

An asset bubble cannot survive without fuel. That fuel is cheap debt. When interest rates are held artificially low for an extended period, money loses its traditional role as a gatekeeper of efficiency. It becomes a commodity to be hoarded and deployed recklessly.

The mechanics of this debt pyramid are visible across multiple sectors.

- Corporate Debt Leverage: Private equity firms acquire historically stable businesses, load them with immense debt obligations to pay out dividends to investors, and leave the operating company with razor-thin margins for error.

- Sovereign Debt Compounding: Governments issue debt to fund current consumption and entitlement programs rather than long-term infrastructure, ensuring that a growing portion of future tax revenue must go purely toward paying interest.

- Consumer Credit Overextension: Stagnant real wages force households to rely on credit cards, auto loans, and buy-now-pay-later schemes just to maintain a middle-class standard of living.

This structural vulnerability magnifies small economic tremors. When debt serves as the foundation for the entire financial apparatus, a slight uptick in default rates can trigger a systemic freeze. We saw this during the subprime crisis, and the underlying architecture has only grown larger and more convoluted since then.

The Real Estate Distortion

Nowhere is this dynamic clearer than in residential and commercial real estate. Housing should function primarily as a utility. It is a place where people live, sleep, and raise families. However, when global capital markets began looking for places to park yield-seeking money, housing was converted into an asset class.

Institutional investors entered neighborhoods, buying up single-family homes with cash. They were not looking to improve communities. They were looking for predictable rental income and capital appreciation. This influx of non-occupant buyers drove home prices far beyond what local wages could support.

When a young family must dedicate 40% or 50% of their gross income to rent or a mortgage, that money is permanently removed from the broader economy. They cannot use it to buy consumer goods, start small businesses, or invest in their own education. The asset bubble in real estate acts as a direct tax on the productive workforce, transferring capital from creators to rent-seekers.

The Productivity Deficit

The ultimate cost of a speculation-driven system is the decay of productivity. True productivity gains are achieved through technological breakthroughs, infrastructure upgrades, and a highly skilled workforce. These require patient capital. Investors must be willing to lock up their money for five, ten, or fifteen years before seeing a return.

Wall Street operates on a ninety-day horizon. Quarterly earnings reports dictate corporate survival. If a CEO announces a massive, high-risk research project that will take a decade to pay off, shareholders often penalize the stock. If that same CEO announces a multi-billion-dollar buyback or a cost-cutting round that fires 10% of the staff, the stock surges.

+---------------------------------------------------------+

| THE Speculative Cycle |

+---------------------------------------------------------+

| Cheap Credit -> Asset Inflation -> Wealth Disparity |

| ^ | |

| | v |

| Bailouts & Liquidity <- Financial Systemic Instability |

+---------------------------------------------------------+

This cycle creates an economy that looks impressive on a spreadsheet but feels brittle on the ground. We see towering valuations for software companies that specialize in optimizing ad clicks, while our electrical grids degrade, bridges crumble, and supply chains fracture at the first sign of geopolitical tension.

Rewiring the Financial Incentives

Fixing this structural imbalance is not a matter of passing a few minor regulations. It requires altering the core incentives that govern capital allocation. The current system socializes losses while privatizing gains, ensuring that speculators take massive risks knowing they will be rescued if the debt pyramid collapses.

Reforming Capital Gains Taxation

The tax code currently favors the speculator over the worker. Income earned through physical or mental labor is taxed at a higher marginal rate than income generated through the sale of an asset held for more than a year. This is a direct subsidy for capital ownership over wealth creation.

A progressive capital gains tax that scales based on the holding period would change behavior. If an asset sold within two years faced a punitive tax rate, while an asset held for ten years received preferential treatment, money would flow away from high-frequency trading and toward long-term corporate bonds and equity investments.

Restricting Share Buybacks

Prior to 1982, the Securities and Exchange Commission viewed open-market share buybacks as a form of stock manipulation. Reinstating strict limits on these transactions would force corporations to find alternative uses for their capital.

If a board of directors cannot simply buy back their own shares to meet earnings-per-share targets, they must invest in product development, expand into new markets, or raise worker wages to attract better talent. All of these outcomes contribute directly to real economic expansion rather than financial engineering.

The Cost of Inaction

Continuing down the path of asset inflation and debt accumulation is a choice with predictable consequences. It widens the wealth gap to a degree that threatens social stability. When young people realize that no amount of hard work can compete with the compounding returns of inherited assets, the social contract breaks down.

The financial system must return to its foundational purpose. It should be a utility that transfers capital from savers to innovators, builders, and operators. When finance becomes the master rather than the servant of industry, the economy stops building a foundation and starts building a countdown.